COVID-19 Real Estate Legal Updates: The Malaysian Government Introduces Special Measures to Revitalise Real Estate Market

The COVID-19 pandemic has dramatic consequences for the Malaysian economy and financial markets, and the real estate market is no exception with mounting pressure on the supply and demand. On 07 June 2020, Prime Minister Tan Sri Muhyiddin Yassin announced that the Conditional Movement Control Order (CMCO) will be replaced with the Recovery Movement Control Order (RMCO) for a phased recovery from coronavirus, commencing with a gradual easing of restrictions and the introduction of new measures to help re-build the Malaysian economy. Since then, the Malaysian government has introduced various economy initiatives to support this move. These include initiatives that are designed to revitalise the real estate market, which are much welcomed by developers, investors, property owners, potential home buyers and landlords. Without further ado, let us take a closer look at these initiatives which are meant to “revitalizing” the real estate market.

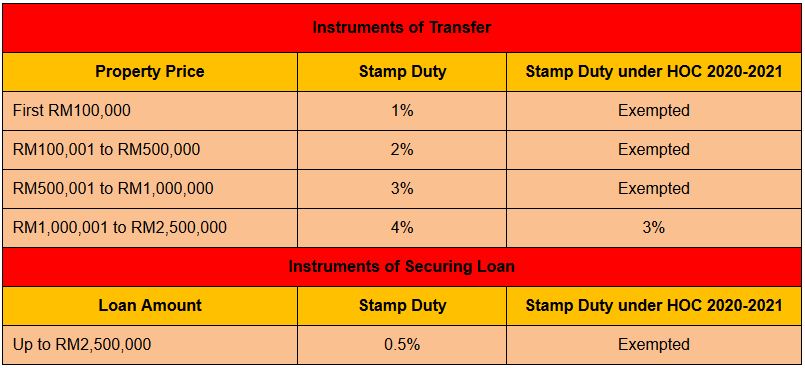

(a) Stamp duty exemptions on purchase of residential property under HOC 2020-2021

What is it all about. Homebuyers will be able to enjoy full stamp duty exemption on the instrument of transfer for residential properties priced up to RM1 million while for properties that are worth more than RM1 million up to RM2.5 million, 3% stamp duty on the instrument of transfer for the amount that is more than RM1 million. On the other hand, full stamp duty exemption is given on instrument of securing loans. Below is a summary of the above:

Eligibility for exemption. Stamp duty exemptions are given for residential properties which are sold during the period between 01 June 2020 to 31 May 2021. The said ‘residential properties’ must be as houses, condominium units, apartments and flats including service apartments and SOHO built and used as dwelling, all other property types are not included in this exercise. The service apartment and SOHO must be for residential use only and cannot be converted for commercial activities. Property price (before discount) is within the range of RM300,000 to RM2.5 million. It must be a sale from a developer to a purchaser or co-purchasers, all of whom are Malaysian citizens. A minimum of 10% discount (from property price) shall be provided by the developer. Those properties must be registered with the relevant authority for each region as follows:

- Peninsular Malaysia: Properties registered with Real Estate & Housing Developers’ Association Malaysia (REHDA).

- Sabah: Properties registered with Sabah Housing and Real Estate Developers Association (SHAREDA).

- Sarawak: Properties registered with Sarawak Housing and Real Estate Developers’ Association (SHEDA).

(b) Stamp duty exemptions on M&A instruments by SMEs

What is it all about. The initiative is created to help local companies build their capacity and encourage the merger of two SME entities or the acquisition of an SME entity by another SME to become a new and larger business entity. The stamp duty exemption will be given for M&A instruments include agreements for the sale or lease of properties (including land, buildings, machinery and equipment); instruments of transfer and memorandum of understanding; loan or financing agreement; and the first lease and/or tenancy agreement.

Eligibility criteria. Application must be validated through the SME Registration Status System, a registration system platform developed by SME Corp Malaysia. Eligible applications are for M&A exercises undertaken from 01 July 2020 until 30 June 2021. The eligibility criteria imposed on the applicants are as follows:

- 100% Malaysian owned; and

- Have annual sales turnover of less than RM50 million or full-time employees of less than 200, as per the definition of SMEs in the manufacturing sector; or

- Have annual sales turnover of less than RM20 million or full-time employees of less than 75, as per the definition of SMEs in the services sector.

(c) RPGT exemption is given up to three (3) residential properties per individual

Following the gazetting of Real Property Gains Tax (Exemption) Order 2020 on 28 July 2020 (“Exemption Order”), an individual is exempted from paying RPGT on the chargeable gain accruing on the disposal of up to three (3) units of residential property if the following conditions are fulfilled:

- the individual must be a citizen who is the sole or joint owner of the property being disposed;

- the property disposed must be a ‘residential property’, namely a house, a condominium unit, an apartment or flat in Malaysia, and includes a service apartment and a small office home office (SOHO) which is used only as a dwelling house;

- the residential property must be disposed on or after 01 June 2020 until 31 December 2021;

- the residential property which is being disposed of is not acquired by way of transfer between spouses; or gift between spouses, parent and child, or grandparent and grandchild where the donor is a citizen; and

- the sale and purchase agreement or the instrument of transfer for the disposal of the residential property is executed on or after 01 June 2020 but not later than 31 December 2021 and is duly stamped not later than 31 January 2022.

Where an individual disposes of more than three(3) units of residential properties, the disposer may elect any three from the said disposals to be exempted and the election so made shall be irrevocable. In the case where the contract for the disposal of a residential property is a conditional contract which requires the approval of the Federal Government or a State Government, the exemption shall only apply if –

- the contract for the disposal of the residential property is executed on or after 01 June 2020 but not later than 31 December 2021 and is duly stamped not later than 31 January 2022; and

- the approval of the Federal Government or the State Government concerned for the disposal of the residential property is obtained on or after 01 June 2020.

It is important to take note that the RPGT exemption given under the Exemption Order does not absolve the disposer from complying with the requirement to submit any returns or information under the Real Property Gains Tax Act 1976.

Comments

The real estate industry and the national economy have a mutual and close tie, and the far-reaching impact. From an economic standpoint, function of real estate industry in the national economy could be reflected from its role in inducing induces direct economic effect, for the other industries such as construction, manufacturing, banking and the professionals that provide services to the real estate industry. Therefore, it is a wise and right decision for the Malaysian government to revitalise and guide the real estate industry via initiatives introduced, so to make this industry continues to play an active role in stimulating economic growth.

** Azmi & Associates is proud to be in collaboration with Henry Butcher Malaysia to work on this piece of legal article entitled “COVID-19 Real Estate Legal Updates: The Malaysian Government Introduces Special Measures to Revitalise Real Estate Market”. Please feel free to click here to download full copy of the newsletter.

Written by:

Zuhaidi Mohd Shahari & Charlie Ng Zheng Hui (general@azmilaw.com)